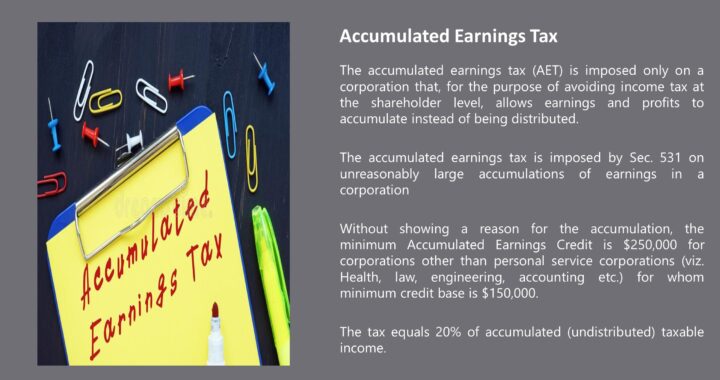

| The accumulated earnings tax (AET) is imposed only on a corporation that, for the purpose of avoiding income tax at the shareholder level, allows earnings and profits to accumulate instead of being distributed. The accumulated earnings tax is imposed by Sec. 531 on unreasonably large accumulations of earnings in a corporation.. |

| Without showing a reason for the accumulation, the minimum Accumulated Earnings Credit is $250,000 for corporations other than personal service corporations (viz. Health, law, engineering, accounting etc.) for whom minimum credit base is $150,000. |

| The Accumulated Earnings Credit (AEC) is deducted from taxable income (TI) to determine accumulated taxable income (ATI) |

| The AET will be imposed regardless of the number of shareholders, provided the corporation does not qualify as a personal holding company. |

| A corporation is liable for the AET when it accumulates (does not distribute) earnings beyond the greater of $250,000 or Reasonable business needs. The tax equals 20% of accumulated (undistributed) taxable income. |

| Taxable Income |

| +/- Adjustments |

| Current E&P |

| – Dividend Paid |

| – AEC |

| ATI |

| * 20% |

| AET |

| The AET is only a tax on ATI (undistributed current year earnings less dividend paid deduction in excess of AEC). However, the undistributed prior year earnings still factor into the calculation of whether total accumulated earnings exceed the accumulated earnings credit or reasonable business needs. |

| The taxpayer is allowed a dividends paid deduction in determining accumulated taxable income for dividends paid after the close of any tax year provided the dividends are actually paid on or before the 15th day of the third month following the year-end. |