Auditing Through The Computer

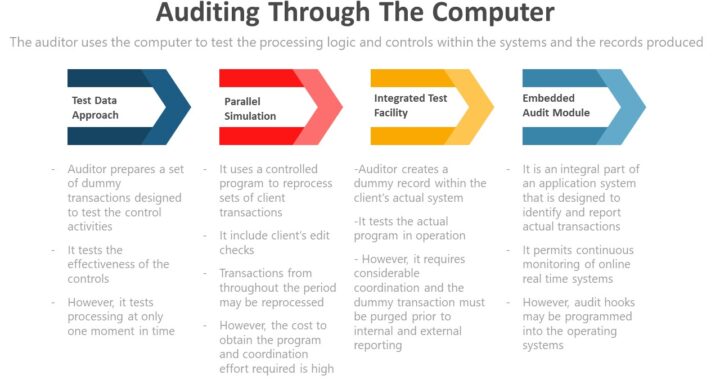

Auditing through the computer – Uses the computer to test the processing logic and controls within the system and the records produced

Test Data Approach – In the test data approach, the auditor prepares a set of dummy transactions specifically designed to test control activities that management claims to have incorporated into the processing programs.

Parallel Simulation – A parallel simulation uses a controlled program (auditor developed program) to reprocess sets of client transactions (real transactions and not dummy) and compares the auditor-achieved results with those of the client.

Integrated Test Facility – Using the integrated test facility (ITF) method, the auditor creates a dummy record within the client’s actual system (e.g., a fictitious employee in the personnel and payroll file). Dummy and actual transactions are processed.

Embedded Audit Module – An embedded audit module is an integral part of an application system that is designed to identify and report actual transactions and other information that meets the criteria of having audit significance (e.g., transactions over $5,000).

If you have found this blog to be useful, you may share with your friends. Thanks!

Purchases-Payables-Cash Disbursement Cycle

Testing of Completeness Assertion for Accounts Payable and Purchases Reconciling total amounts in subsidiary ledgers with the general ledger Performing analytical procedures (e.g., comparing accounts payable turnover with the previous year) Tracing subsequent payments to recorded payables Searching for unvouchered (unsupported) payables Testing of Accuracy Assertion for Accounts Payable and Purchases Obtaining management representation letters […]

Continue reading

Payroll Responsibilities

Duty Department/Individual Provides authorizations of employees and their pay rates – Human resources Oversees employees’ working hours (time cards) – Timekeeping Prepares the payroll register – Payroll Prepares payment vouchers – Accounts payable Approves the payments (signing checks) – Cash disbursement (CFO) Records the payrolls – General ledger If you have found this blog to […]

Continue reading

Electronic Data Interchange

Electronic Data Interchange – EDI is the communication of electronic documents directly from a computer in one entity to a computer in another entity. The advantages of using EDI are: Reduced clerical errors Increased speed Elimination of repetitive clerical tasks Elimination of document preparation, processing, filing, and mailing costs An audit trail allows for the […]

Continue reading

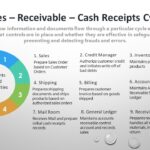

Sales – Receivables – Cash Receipts Cycle

Completeness assertion for sales and receivables Reconciling total amounts in subsidiary ledgers with the general ledger Performing analytical procedures (e.g., comparing accounts receivable turnover with previous year) Accounting for the numerical sequence of sales orders, shipping documents, and invoices Tracing from sales invoices to shipping documents Accuracy assertion for sales and receivables Obtaining management representation […]

Continue reading

IT Controls – General and Application Controls

Types of Controls and Scope General controls – The organization’s entire processing environment Application controls – Particular to each of the organization’s applications Three Categories of Application Controls are: Input controls Processing controls Output controls Three types of controls classified by function are: Preventive controls Detective controls Corrective controls Input controls provide reasonable assurance that […]

Continue reading

Components of Internal Control

Three Objectives of Internal Control are: Operations —- Effectiveness and efficiency of operations Reporting — Reliability of financial reporting Compliance — Compliance with applicable laws and regulations 5 Components of Internal Control are: Internal controls stop CRIME Control activities Policies and procedures Risk assessment process Identification and analysis of relevant risks Information system Information systems […]

Continue reading

Audit – Strategic Planning Issues

Documentation of Audit Plans include: The overall audit strategy (basis of the audit plan) Procedures to be performed Risk assessment procedures Further procedures Other procedures Involvement of specialists Three aspects of audit procedures should be documented in audit plans are: NET of procedures N = Nature E = Extent T = Timing Factors external auditors […]

Continue reading

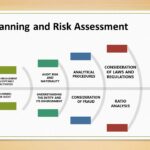

Audit Planning and Risk Assessment

[A] Pre-Engagement Acceptance Responsibilities 1) Preconditions for an Audit – Auditor to determine that management uses Acceptable financial reporting framework Understands its responsibility for the preparation and fair presentation of financial statements Understands its responsibility for the design, implementation and maintenance of internal control and Understands its responsibility to provide access to all information 2) […]

Continue reading

Professional Responsibilities

AICPA Code of Professional Conduct has a set of specific mandatory rules describing minimum levels of conduct a member must maintain as a CPA Profession has a responsibility to the public. AICPA Code of Professional Conduct expects the CPA to honour public trust Rules that are mandatory for all members are : (a) Integrity and […]

Continue reading