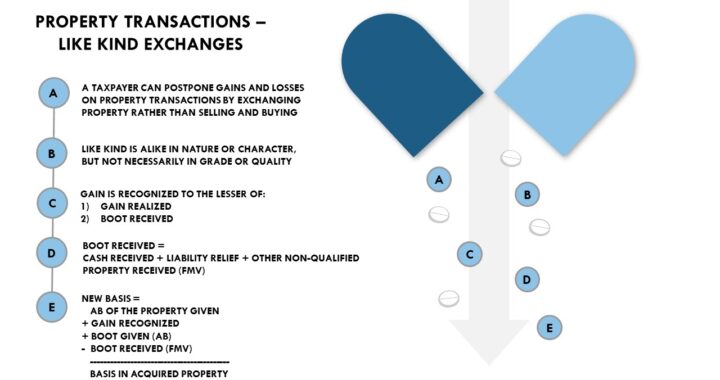

Section 1031 defers recognizing gain or loss to the extent that real property productively used in trade or business or held for production of income (investment) is exchanged for property of like kind. Only real property qualifies for like kind exchange.

Like-kind refers to the nature or character of the property. Real estate for real estate qualifies as a like-kind exchange even if the properties are as different as a rental office building and a parking lot, or even if the properties are located in different states. All other property, including stocks (and other securities and debt instruments) and partnership interests, is excluded from qualifying for like-kind exchange treatment.

Boot is all nonqualified property transferred in an exchange transaction. Boot received includes cash, net liability relief, and other nonqualified property (its FMV).

Recognized Gain = Lesser of gain realized or boot received

Deferred gain = Realized gain – Recognized gain

Deferred loss = Realized loss

Basis of acquired property = AB of property given + Gain recognized+ Boot given – Boot received

OR

Basis of acquired property = FMV of acquired property – Deferred gain + Deferred loss

If you have found this blog to be useful, you may share with your friends. Thanks!