Three Objectives of Internal Control are:

Operations

—- Effectiveness and efficiency of operations

Reporting

— Reliability of financial reporting

Compliance

— Compliance with applicable laws and regulations

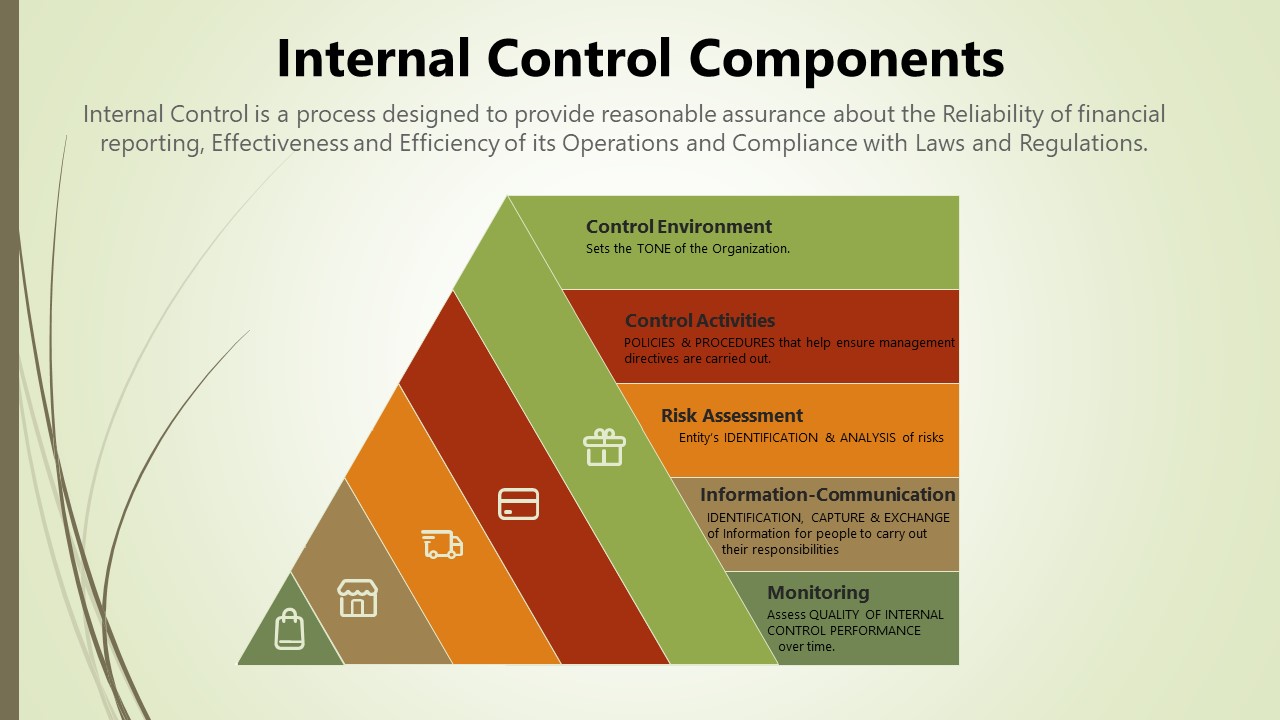

5 Components of Internal Control are:

Internal controls stop CRIME

Control activities Policies and procedures

Risk assessment process Identification and analysis of relevant risks

Information system Information systems and communication

Monitoring of controls Assessment of control effectiveness over time and corrective actions

Control environment Tone at the top and control consciousness of members

Internal controls provide only reasonable assurance, but not absolute assurance, that an entity’s objectives are met.

Inherent Limitations of Internal Control are:

Human error (e.g., faulty human judgment)

Collusion

Management override

Cost and benefit constraint

If you have found this blog to be useful, you may share with your friends. Thanks!