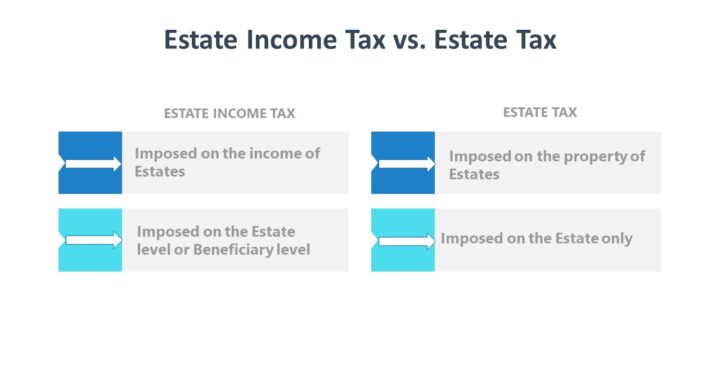

Estate Income Tax

Estate Income Tax – Imposed on the income of estates. Imposed on the estate level or beneficiary level

An estate (or trust) with a gross income of at least $600 is required to file Form 1041, Income Tax Return for Estates and Trusts, no later than the 15th day of the 4th month following the close of the entity’s tax year.

Neither trust nor an estate is allowed a standard deduction on the fiduciary income tax return. A personal exemption deduction, however, is allowed: $600 for an estate; $300 for a simple trust; $100 for a complex trust.

The distinction between the trust or estate income and the principal is an important one. Tax is imposed on the taxable income (TI) of trusts or estates, but not on items treated as fiduciary principal. The Revised Uniform Principal and Income Act specifies that certain items, including business income, interest, rents, and taxable dividends, are to be treated as income to the trust or estate. The act also lists certain items to be treated as principal, including consideration for property (e.g., gain on sale), stock splits, stock rights, and liquidating dividends.

Administration expenses (and debts of a decedent) are deductible on the estate tax return, and some may also qualify as deductions for income tax purposes on the estate’s income tax return. Double deductions are disallowed. A waiver of the right to deduct them on Form 706 is required in order to claim them on Form 1041.

Similar to individuals, the taxable income of trusts and estates is the excess of gross income over deductions.

Gross Income

Capital gains are taxed. Income in respect of a decedent is taxed as income Life insurance proceeds are excluded from income

Deduction

Expenses attributable to tax-exempt income are not deductible. A capital loss is deductible to the extent of capital gains plus $3,000. Personal Exemptions are available.

Losses from a passive activity cannot be used to offset portfolio income

Deduction for Distribution = Allocates taxable income of the trust between Trust and the beneficiary. The deduction is lesser of:

a) Amount of required distributions; or

b) Distributable Net Income

Estate Tax

Estate Tax – Imposed on the property of estates. Imposed on the estate only

A decedent’s gross estate includes the FMV of all property, real or personal, tangible or intangible, wherever situated, to the extent the decedent owned a beneficial interest at the time of death. Included in the gross estate are such items as cash, personal residence and effects, securities, other investments, and other personal assets, such as notes and claims and business interests.

A decedent’s gross estate includes property held jointly at the time of the decedent’s death by the decedent and another person with the right of survivorship.

The gross estate includes assets transferred during life that, at death, the decedent retained the power to revoke, such as transfers made to a revocable trust.

The executor can elect to value the estate at the FMV on

The decedent’s date of death

6 months after the decedent’s death

Deductions from Gross Estate

Expenses for selling property of the estate if the sale is necessary (1) to pay the decedent’s debt, (2) pay the expenses of estate administration, (3) pay taxes, (4) preserve the estate, and (5) effect distribution

1) Administrative and funeral expenses

2) Claims against the estate (e.g., debts of the decedent)

3) Unpaid mortgages on the property

4) State death taxes

5) Casualty or theft losses

6) Charitable contributions

7) Marital transfers