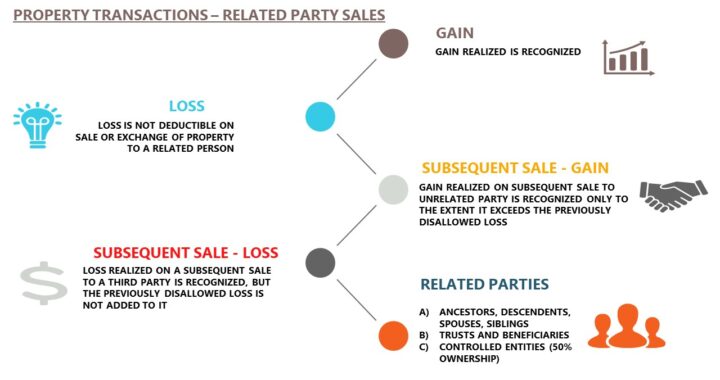

Limited Tax Avoidance Rules limit tax avoidance between related parties.

Gain recognized on an asset transfer to a related person in whose hands the asset is depreciable is ordinary income.

Loss realized on the sale or exchange of property to a related person is not deductible.

Under Sec. 267, losses are not allowed on sales or exchanges of property between related parties. However, the Sec. 267(d) disallowed loss is used to offset the subsequent gain on the sale of the property.

Related Parties include:

Ancestors, descendants, spouses, and siblings

Trusts and beneficiaries of trusts

Controlled C corporations, S corporations, and partnerships (greater than 50% direct or constructive ownership)