The objective of segment reporting is to provide information about the different business activities of the entity and the economic environments in which it operates.

An operating segment has three characteristics:

- It is a business component of an entity that may recognize revenues and incur expenses

- Its operating results are regularly reviewed by the entity's chief operating decision-maker

- Its discrete financial information is available

Operating segments may be aggregated if:

- Doing so is consistent with the objective;

- They have similar economic characteristics; and

- They have similar products or services, production processes, classes of customers, distribution methods, and regulatory environments

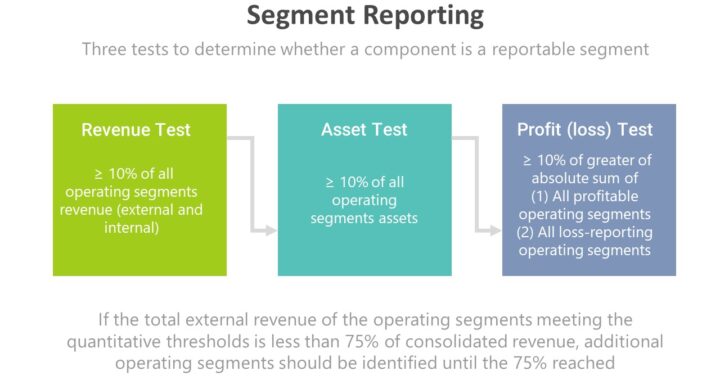

Quantitative Thresholds

Reportable Segments are operating segments that must be separately disclosed if one of the following quantitative thresholds are met:

Test Amount Percent of Relevant Amount

Revenue >= 10% of all operating segments

Assets >= 10% of all operating segments

Absolute Profit or Loss >= 10% of greater of the absolute sum of

1) all profitable Operating Segments or

2) all loss-reporting Operating Segments

If the total external revenue of the operating segments meeting the quantitative thresholds is less than 75% of consolidated revenue, additional operating segments are identified as reportable until the 75% level is reached

Information about nonreportable activities and segments is combined and disclosed in an all other category as reconciling item

If you have found this blog to be useful, you may share with your friends. Thanks!