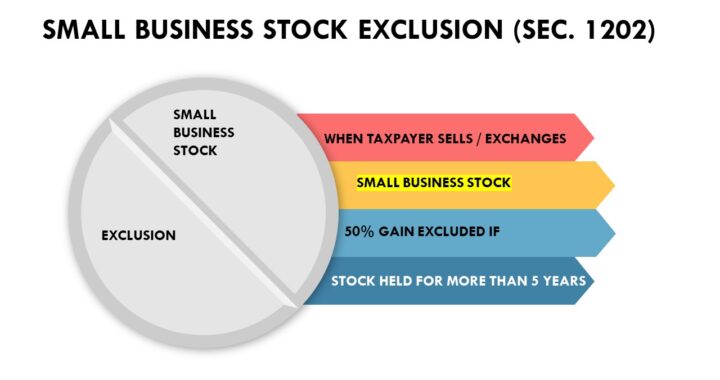

Stock qualifies as Section 1202 stock if it is received after August 10, 1993, the corporation is a domestic C corporation, the seller is the original owner of the stock, and the corporation’s gross assets do not exceed $50 million at the time the stock was issued. Additional requirements do exist. However, the total gross assets requirement is $50 million.

Under Sec. 1202(a), an individual may exclude from gross income 50% of any gain from the sale or exchange of qualified small business stock held for more than 5 years. The exclusion increased to 75% for purchases between February 17, 2009, and September 28, 2010, and 100% after that.