Taxable Income = AGI – Itemized Deduction on Schedule A or the standard deduction – QBID

Standard Deductions

Persons who are not allowed Standard Deductions are:

1) Persons who itemize deductions

2) Nonresident alien individuals

3) Individuals who file a “short period” return

4) Married individuals who file a separate return and whose spouse itemizes

5) Partnerships

6) Estates or Trusts

The standard deduction is the sum of the basic standard deduction and the additional standard deduction.

Standard Deduction Limits for 2020 are:

Married Filing Jointly / Qualifying Widower – $24,800

Head Of Household – $18,650

OTHERS – $12,400

An additional standard deduction ($1,650) is allowed for a taxpayer if, during the year, the taxpayer is age 65 or over or blind. The respective amounts are doubled if the taxpayer is both elderly and blind.

The basic standard deduction amount of a student under age 24 who is claimed as a dependent on another individual’s income tax return is limited to the greater of either $1,100 or the dependent’s earned income for the year plus $350 up to the otherwise applicable basic standard deduction amount. Earned income does not include either dividends or capital gains from the sale of stock

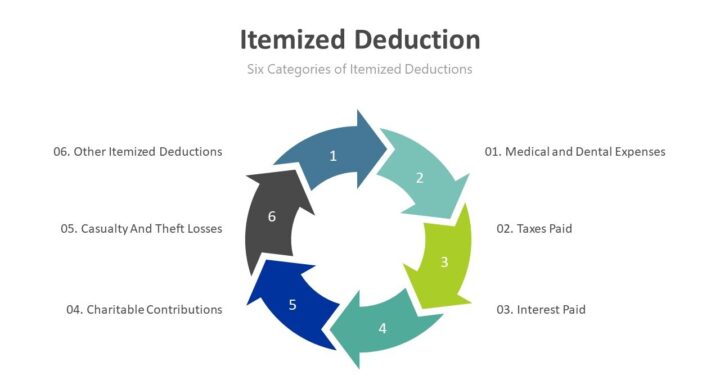

Itemized Deductions

The six categories of itemized deductions are:

1) Medical and dental expenses

2) Taxes paid

3) Interest paid

4) Charitable contributions

5) Casualty and theft losses

6) Other itemized deductions