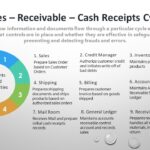

Completeness assertion for sales and receivables Reconciling total amounts in subsidiary ledgers with the general ledger Performing analytical procedures (e.g., comparing accounts receivable turnover with previous year) Accounting for the numerical sequence of sales orders, shipping documents, and invoices Tracing from sales invoices to shipping documents Accuracy assertion for sales and receivables Obtaining management representation […]

Continue reading