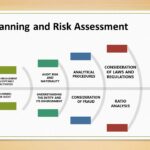

Testing of Completeness Assertion for Accounts Payable and Purchases Reconciling total amounts in subsidiary ledgers with the general ledger Performing analytical procedures (e.g., comparing accounts payable turnover with the previous year) Tracing subsequent payments to recorded payables Searching for unvouchered (unsupported) payables Testing of Accuracy Assertion for Accounts Payable and Purchases Obtaining management representation letters […]

Continue reading