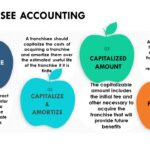

A franchise is a contractual agreement by a franchisor to permit a franchisee to operate a certain business Franchisee Accounting The franchisee should capitalize the costs of acquiring the franchise such as the initial fee and other expenditures (eg. legal fees) incurred to acquire the franchise Franchise costs are amortized over their estimated useful life […]

Continue reading