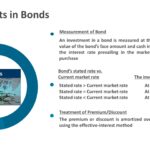

A bond is a formal contractual agreement by an issuer to pay an amount of money (face amount) at the maturity date plus interest at the stated rate at specific intervals. All items are stated in a document called an indenture The investor in a bond may elect FVO since the bond is a financial […]

Continue reading