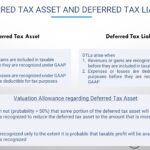

The asset and liability approach is used to account for income taxes The tax consequences of some transactions or events may be recognized in income taxes currently payable or refundable in a year different from that in which their financial statement effects are recognized (temporary differences) Also, some transactions or events may have tax consequences […]

Continue reading